|

In this post, I'm going to show you that Financial Statements aren't difficult to understand and how everyone can get the information they need.

Whether your an employee or an employer the financial statements of the business you work in effect your job and subsequently your personal life. So you would think one of the basic things we would learn at high school is how to read them. But surprisingly it's not always the case.

So it becomes one of those mysterious pieces of information that we think only "clever" people understand or we say "My accountant looks after that for me".

So many of us have or will go through the following scenario. We're working at our job. We hear rumours that the business may not be doing so well but we're not sure, more rumours fly around creating uncertainty. Rumours of potential job losses swirl around the office or yard. We get nervous, what's happening, we're not sure. No ones keeping us informed.

Then the first we hear there's an official problem with the business is you lose your job. It's gut-wrenching. What I always found more frustrating was why wasn't I told there was a problem within the business? Why was it kept a secret? The answer is they fear you will go before they want you to leave.

Now, let's go back 12-18 months and let's run a different scenario.

The company has open book management in place, you have weekly meetings where the MD and the management teams run through the companies financials. He and the management team identify a cash flow problem. Staff are aware of what this means and they know what causes it.

The staff propose to hold less inventory. Also to order less but more often. They pay slightly more but inventory is turning over much more quickly. The admin team will double their efforts to chase down late payers. We ask key suppliers for an extra 30 days payment terms for the next 3 months. The warehouse team set-up an eBay store and start to eBay or the old return stock and package damaged stock turning it in cash. Old and slow-moving stock is reduced and turned into cash and not re-ordered.

As you can imagine the outcome is very different from the first scenario where the first we knew officially of trouble in the business is when we lost our job.

We have not only saved our job but the business is in a better position than it was 12 months ago, a win, win scenario.

So let's look at the two key financial statements you need to know. Balance Sheet and Profit and Loss.

Balance Sheet

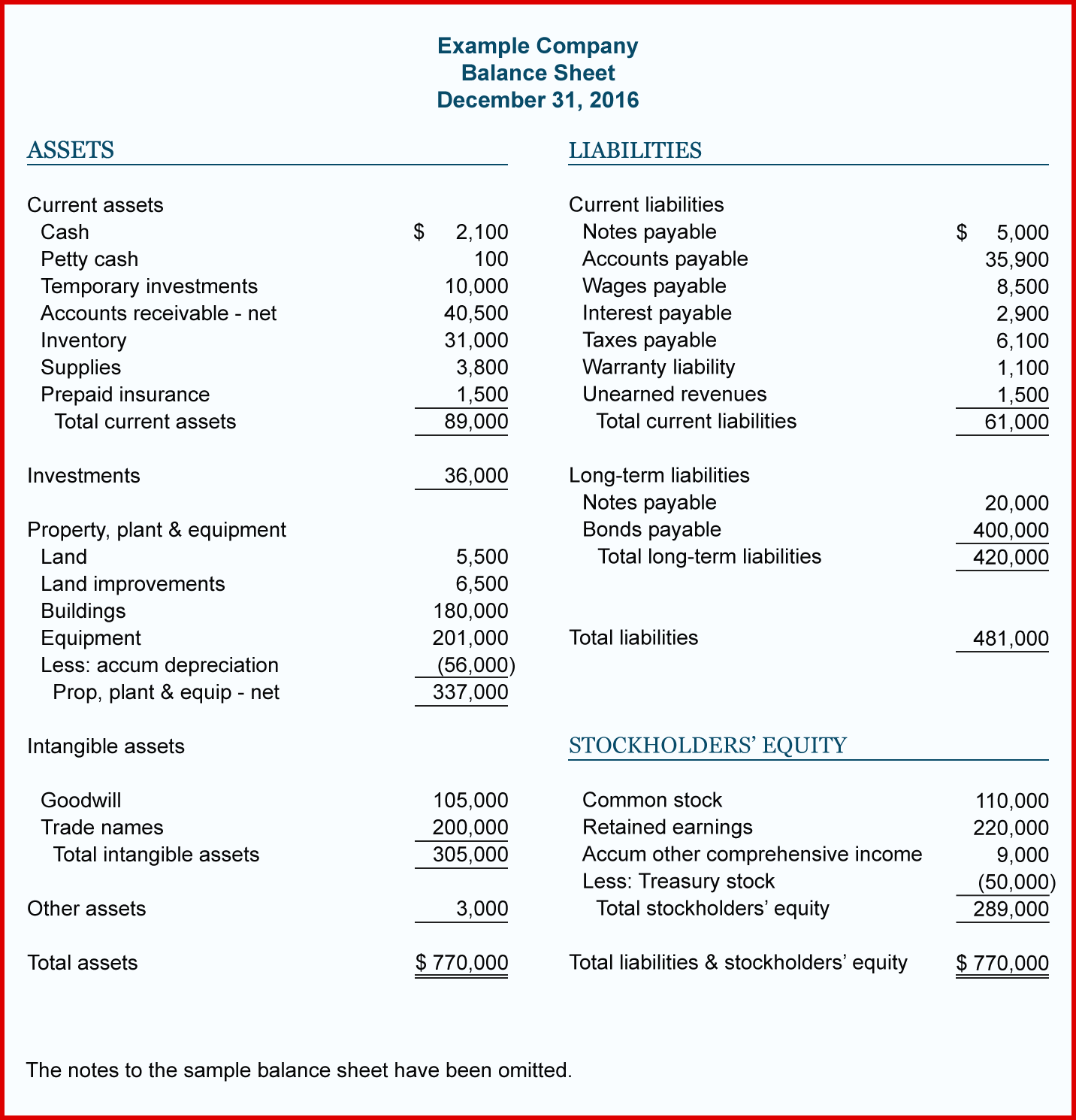

The balance sheet tells you overall how your business is doing. It tells you how liquid you are, your overall financial well being. The key number from the balance sheet is called the Ratio or Current Ratio as it can also be called. Key to note is its only a snapshot of that day in time. But will give you a good general idea of the state of the business.

You can run a balance sheet from any accounting software package. No matter the size of your business you need accounting software. Don't ever think my business is too small, just for the ease of running an accurate Balance Sheet and Profit and Loss report. It's invaluable. Xero and Quick Books are the most common.

To calculate the ratio you need the Current Assets total. Current Assets are things in your business that can be turned to cash within 12 months. Usually consists of your bank accounts and stock or inventory.

Then you need your current liabilities. This is debts the business will need to repay in the next 12 months. In here will be supplier invoices, overdrafts, short terms loans, interest, pension commitments etc.

The Ratio formula is simply Current Assets divided by Current Liabilities. Simple! What this basically means is do you have enough liquid assets to cover your debts for the next 12 months. Basically how healthy is the business? There are lots of numbers on the balance sheet and much information can be taken from it, but the Ratio is all that's needed.

Ideally, you want to see the number above 2. This means you have twice as much liquidity compared to what you owe. A healthy place to be. A negative number means you don't have enough cash or liquid assets in the business to cover what you owe. This is a concern, not a disaster but you need to pay immediate attention to this number and put plans in place to remedy this.

Here is an example of a Balance Sheet.

|